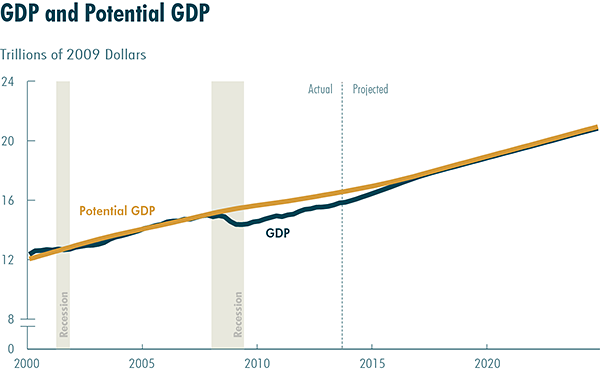

The global economy faces a weak pattern of effective demand, due to a slowdown in China and commodity exporting countries and an unsuccessful export-based recovery in Europe. That trend will constrain US growth and deteriorate the US external position, according to the The Kingston Financial Balances Model (KFBM) Weak global demand and slowing US growth at an average annualized rate of 2.4% are the cornerstones for the baseline scenario. Based on that we projected a US current account deficit of 4.0% by the end of 2018 corresponding to a trade deficit of 4.3% or $900 billion says the latest newsletter based on the model.Download the full KFBM report. Up to the eighties, the US economy was characterized by a balanced current account, even enjoying minor surpluses in individual years. Since then, the current account has been in a chronic deficit position, peaking at 6% of GDP just before the crisis of 2007-2008. The ability of the US to finance these sustained current account deficits depends on the US dollar and its dominant role. In an alternative scenario the model explores the effect of an appreciation of the US dollar and a further slowdown in global GDP growth. The result is a current account deficit of 4.7%, a trade deficit of 5%, which implies a 1.4% private sector deficit, magnitudes only seen between 1998 and 2001 and in 2007, episodes which preceded situations of great financial distress. Financial forecasting can be as perilous as trying to predict the weather, but researchers at Kingston University London have developed a new way to more accurately assess the outlook for the world’s biggest economy. The new model highlights the interdependence of household, business and government expenditure and international trade in the United States and is rooted in a new approach to economics teaching. Studying economists have predominantly been taught one theory; Neoclassical economics. However, since the global financial crisis hit the headlines in 2008, students across Britain have increasingly been calling for reform in the way their subject is taught. “The crash showed the weaknesses in Neoclassical economics - we need to hear more than one theory,” Kingston University PhD candidate Rafael Wildauer, who developed the model in collaboration with fellow PhD candidate Javier López Bernardo, explained. “Kingston University has already responded to post-crash shifts in economic thinking, teaching Keynesian and post-Keynesian theory as an alternative to mainstream classes. This way of thinking is increasingly important,” he said.

Kingston University PhD candidate Rafael Wildauer., Credit: Kingston University

This reformed approach is evident in the financial balances model, designed to assess the sustainability of current to medium term trends in the American economy. The Kingston Financial Balances Model (KFBM) is built around the idea that the financial balances of different sectors are all relevant for an understanding of the evolution of the economy as a whole. The model breaks down the economy into three sectors – the private sector balance is the expenditure of households and firms; the public account balance is the revenue and expenditure of federal and local government; and the current account balance is the revenue and expenditure between the US and the rest of the world, with trade the most important part. “The financial balances approach is different from what is traditionally taught in a macroeconomics class,” Mr López explained. “We rely on the simple but powerful insight that the expenditures of one sector are the revenues of another – a fact often overlooked in standard macroeconomic models. Other models don’t have this structure. Some look at household expenditures but don’t look at trade, for example. We consider all sectors of the economy together – so if households are saving, what does this mean for the corporate sector?” The KFBM uses United States Congressional Budget Office (CBO) forecasts of GDP, government expenditures and revenues until 2018 to predict the public account balance. The current account is forecast based on a statistical model which relies on CBO data, and the private sector balance is derived as the residual between the current and public account.

“The inter-relatedness of the sectors means that if a government administration chooses a certain fiscal path – trying to reach a particular reduction in the public deficit, for example – this has a profound effect on other sectors of the economy,” Mr Wildauer said. “Governments can only really decide expenditures, and this does not seem to be properly recognised – particularly by the media.” Kingston University’s Head of Economics Steve Keen is a leading voice in demanding the reform of economics teaching to encompass more relevant applicable theories. He places great importance on giving colleagues the freedom to develop new ways of working. “We teach economics as if money really matters—which mainstream economics doesn’t do,” said Mr Keen. “We have a sufficient number of staff embracing new thinking to develop alternative approaches. We analyse the economy as if it can be out of equilibrium, where mainstream thinking assumes stability.” The first KFBM report, published in February, predicted a baseline current account deficit of 4 per cent, leading to an increased deficit of 4.7 per cent by the end of 2018. According to the report, global demand is likely to remain weak in the medium term due to a troubled Chinese economy, low growth in commodity-exporting countries due to low prices, and an unsuccessful export-

Comparison between U.S. states and countries by GDP in 2012 , Credit: Ali Zifan

focussed recovery strategy in Europe. A negative financial balance of the US private sector has only been seen prior to the financial crises of 2001 and 2006, Mr López explained. “Although US private sector deficits might continue to support national and global growth rates in the short-run, there is a lack of worldwide demand and already high private sector debt levels,” he said. “The KFBM report concludes sustained economic expansion in the United States is highly unlikely.” Mr Keen was impressed with the findings. “I like the conclusions of the report,” he said. “Just as savings affect cash flow, this applies to current trends. What this leads to is an impossibility of sustained growth in the US economy.” The next KFBM report is due to be published in September. Mr Wildauer and Mr López plan to use the next tranche of data to examine what the forecasts imply for American unemployment figures. They also hope to model households and businesses separately to make the findings more accurate. An unrelated but nonetheless interesting map of the U.S. states economies compared to countries in GDP.

- Contacts and sources:

- Kingston University London, \

- Source: http://www.ineffableisland.com/